Given the findings of the Independent Review, and particularly the highly controversial Interim Report (which essentially called for the NSW Government to legislatively override existing toll concession agreements, causing heart attacks at Transurban and among its investors), the recommendations to finally come out of this review are critical. However, equally critical is what, if anything, the NSW Government is going to do in response.

It's worth noting the wealth of data and research compiled in this review, which should help inform discussion and debate about tolling in Sydney for some time.

42 recommendations were made, and I wont repeat them all in detail here.

However, a key part of the review work was to model the impacts of models of reform that were presented. It's critical to understand that the report recommends "moving towards" the Network Toll Restructure and Reduction model, not necessarily the details of that model exactly, but does not recommend the Network Toll Restructure Model. Therefore, I will focus on the former.

These models are:

• Network Toll Restructure model: Introduction of standardised network tolls and including application of two-way tolling; and

• Network Toll Restructure and Reduction model: This uses revenues generated from two-way tolling, peak pricing and other sources to reduce tolls where appropriate. A declining distance approach with fixed infrastructure charges is proposed.

The effect of the latter was modelled as meaning:

• 78% of motorists are the same or better off, 17% would pay $3 + more per trip.

• Main losers are those using the Sydney Harbour Crossings

• Western Sydney motorists get some relief as longer trips are reduced in cost

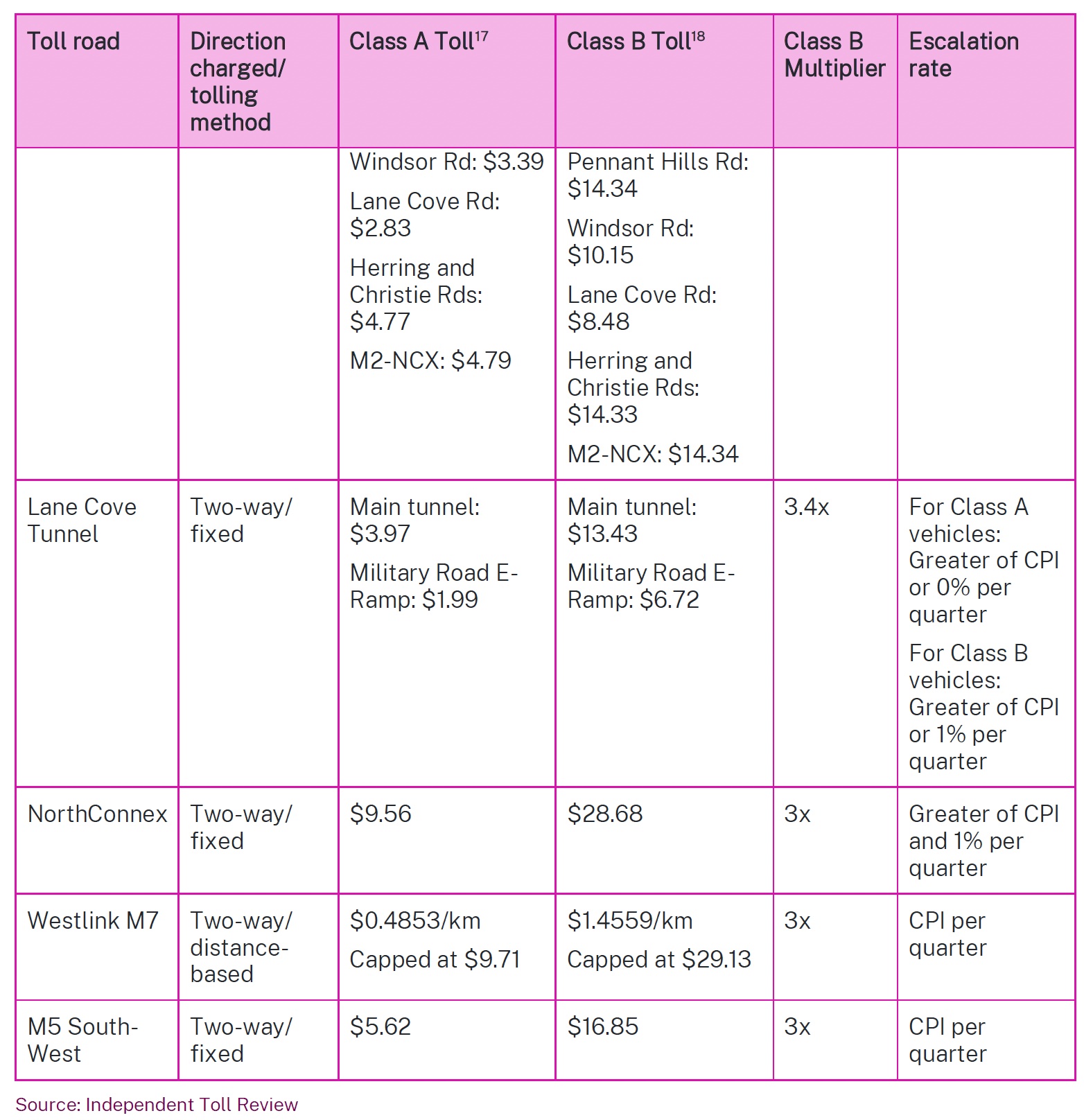

The following table lists the current tolls in Sydney (all in Australian Dollars ~ US$0.66-A$1.00:

It's striking that the obvious impacts on reducing traffic are on the Harbour Crossings and Eastern Distributor, as introducing northbound tolls on the Harbour Crossings and southbound on the Eastern Distributor sees some redistribution of traffic to the west, primarily on the untolled crossing at Iron Cove Bridge and Gladesville. There is also reduction on some streets in the CBD and some parallel routes to the M5, as lower tolls make some toll roads more attractive that local streets for some drivers. The M4 and M5 in particular see much higher traffic volumes. It's unclear the impact on congestion overall, as this did not include any peak/off-peak pricing on a network basis.

This table produced with the press release accompanying the Independent Toll Review (PDF) illustrates the effects on some toll trips:

Before summarising the other recommendations, it is worth going over in some detail the proposed tolling principles (the first set of recommendations).

Tolling principles

These principles are recommended to guide policy measures to reform tolling of existing roads and should inform the implementation of tolling on new roads.

The Tolling Review considered the set of tolling principles agreed in 2014 which were as follows:

1. New tolls are applied only where users receive a direct benefit.

2. Tolls can continue while they provide broader network benefits or fund ongoing costs.

3. Distance-based tolling for all new motorways.

4. Tolls charged for both directions of travel on all motorways.

5. Tolls charged reflect the cost of delivering the motorway network.

6. Tolls take account of increases in expenses, income and comparable toll roads.

7. Tolls will be applied consistently across different motorways, to the extent practicable, taking into account existing concessions and tolls.

8. Truck tolls at least three times higher than car tolls.

9. Regulations could be used so trucks use new motorway segments.

10. Untolled alternative arterial roads remain available for customers.

The review found that these were rather general and didn’t include some key issues, such as the proportion of costs that should be recovered from tolls relative to taxpayer funds. There was little recognition of the need for tolls to vary by time of day, plus although some of the principles (tolling in both directions) are valid, they were not always applied (see the Harbour Crossings and Eastern Distributor).

The review proposed a set of modified principles with one set about the level and structure of tolls and another on consistency with competition policy.

Proposed New Tolling Principles

On the level and structure of tolls:

• Toll setting should be guided by the objectives of efficiency, fairness, simplicity and transparency.

• Tolls should have regard to the costs associated with the provision of toll road services as well as benefits. Declining distance-based tolls are consistent with the principle and have efficiency and equity advantages over fixed distance-based tolls or variable zonal distance-based tolls.

• In general, it is appropriate that beneficiaries pay for toll roads, for example, where benefits flow to the broader community then government contributions are appropriate. The extent of cost recovery achieved through tolls should reflect the extent to which a toll road’s benefits are enjoyed directly by motorists.

• The process for setting tolls should be transparent to the public to promote understanding and allow for informed comment.

• The methodology for determining tolls should, so far as possible, be applied consistently across the entire network.

• Tolls should allow toll road operators to recover their costs incurred in financing the construction of the toll road including an appropriate (i.e. risk adjusted) return, and efficient operating and maintenance costs where relevant. It may be appropriate to apply specific charges to individual parts of the network to allow for cost recovery, for example infrastructure charges to cover the additional costs associated with constructing tunnels or bridges.

• Tolls should not be set at a level which would allow excessive, monopoly profits, or inefficient cost levels to prevail over time.

• Maintaining flexibility to adjust tolls over time in response to demand and supply changes is important.

• Toll setting should take into account fairness as well as efficiency considerations, bearing in mind that other more direct policy approaches may be preferable forms of intervention in relation to fairness.

• The different vehicle categories for tolls should balance impactor pays (the extent to which vehicles impose costs on the network and other users due to their weight and size set against the costs imposed by such vehicles on ancillary roads) and beneficiary pays considerations (a higher willingness to pay for travel time savings). For example, under this principle setting higher tolls for heavier and larger vehicles is consistent with efficient tolling.

• The structure of tolls should be simple enough to be readily understood by users and avoid creating perverse incentives for the use of the road network. Inconsistent approaches to the tolling of toll roads can cause distortions to traffic flows.

• Tolling information should be communicated in real time to inform customer journeys and enable improved decision-making.

On consistency with competition policy:

• Competitive pressure should be harnessed when setting tolls and assessing concessionaire bids (competition for the market) and when regularly reviewing tolls (competition in the market). Bidding for concessions should focus on ensuring tolls are set at competitive levels.

• Unsolicited proposals for toll road extensions should not be considered in isolation of the possibility of first modifying tolls to better manage traffic flows.

• Restrictions should not be imposed on the use of any road or public transport in order to enhance the financial viability of a toll road.

• Tolls should only apply where motorists have reasonable and effective untolled road options, including arterial roads, or public transport alternatives, except where community benefit may necessitate restriction on access to alternatives.

Other recommendations

Moving to network tolling: The core recommendation is to change the current ad-hoc setting of tolls by individual concession (and the State), to a more coherent and consistent approach. The key recommendation is to have declining distance-based tolls, so that the first two kilometres are charged at a higher rate than the next two and so on. This is for fairness, but also efficiency to recognise the cost imposed on other users of using toll roads for shorter trips, and disrupting traffic flow. Network tolling should mean some reductions in tolls, through measures like implementing two-way tolls on one-way toll roads, and more use of peak tolling to lower tolls off-peak. Moving to network tolling should help with steps to phase out or reform toll relief, and how to progress this over time. Other options to lower tolls includes extending toll concessions.

Using pricing to influence demand: Going beyond tolling as an infrastructure cost recovery measure, is to use peak and off-peak pricing, with an initial focus on trialling peak pricing for the freight sector. This is both to reduce congestion at peak times, and to encourage better use of spare capacity off-peak. Included in this recommendation is dynamic pricing, which by the conventional definition is not a good idea in this context (although reviewing peak/off-peak pricing more frequently than annually IS a good idea).

Updating vehicle classifications and charges: Having uniform classifiers and consistent multipliers for heavy vehicles are the key recommendations, along with exempting public bus services from all (not just some) toll roads.

Expanding toll coverage: Applying two-way tolling on the Sydney Harbour Crossings and Eastern Distributor is the obvious step (and one that has generated understandable controversy in isolation). More strategically, the review recommended evaluating the entire motorway network to see if untolled sections should be tolled (reducing tolls on other sections) or if tolls should be removed from some sections. It seems likely that this will be difficult to sell politically.

Initial assessment of toll reforms: Implementation of the reforms should be carefully monitored with frequent modelling to ensure results meet policy objectives.

NSW Motorways: The review recommended establishing a new entity called NSW Motorways, intended to strengthen governance and accountability over NSW toll roads in order to improve outcomes and transparency for motorists. It would work with concessionaires to set network tolls and adjust them working with concessionaires. It would take over the E-Toll retailing business of Transport for New South Wales and have a focus on innovating to improve the tolling experience in the state. It could also manage future toll roads and contract managers for those toll roads, and bring existing public toll roads within its operations.

Concessionaire negotiations: The Review recommends that the Government negotiate with concessionaires to implement network tolling by the end of 2024 and if not achieved, use legislation to advance it. This raises obvious concerns about legislating over the contracts the state has with concessionaires.

Independent oversight of toll setting: The Independent Pricing and Regulatory Tribunal (which is already price regulator for water, public transport and local government services) should also have oversight for toll rate setting. It should work with NSW Motorways and Transport for New South Wales to monitor prices, including the financial and traffic impacts of network tolling, toll relief schemes, the need for and operation of time-of-day pricing and concessionaire performance.

Legislative package for toll setting: Essentially a recommendation to legislate over concession agreements if necessary to implement network tolls. This should include a Revenue Adjustment Mechanism so revenues can be “appropriately” shared.

Competition measures: These recommendations seek more competition in future concessions and a long-term view on competition with procurement of future toll roads. Concession periods should be set based on public interest considerations, including competition. Competitive tendering should be favoured over unsolicited proposals. Roaming fees (across retail toll providers) should be regulated.

Transparency for motorists: Motorists should be able to see past and projected future toll road spending. More information should be provided for trip-planning online and via apps, as well as better signage to inform motorists of toll road prices before they make a decision on whether or not to use a toll road.

Tolling customer advocate: NSW Motorways should have a tolling customer advocate function to consider and manage customers complaints, influence improvements to systems, processes and legislation to minimise future complaints and improve compliance. It should manage awareness and education campaigns, address new “pain points” from the transition to network tolling, and publish reports on the implementation of toll reform. If a toll debt is disputed, debt recovery action should be suspended while the dispute is being addressed.

Industry ombudsman: Proposes that NSW, Victoria and Queensland require toll operators to belong to a statutorily approved independent dispute resolution scheme.

Toll notices: These should be simplified and modernised, calling them “invoices” and removing administration notices, but adding late payment fees to incentivise early payment. Information provided should be user-centric, informing them of the most common reasons for non-compliance (flat tag battery and number plate not linked to an account) so motorists can address such issues to avoid a repeat of unpaid tolls.

Debt recovery: Reform criminal enforcement so there is only one offence per trip and clearly identify if it applies to the driver or the registered vehicle. At present debt is owed by the vehicle’s owner, but it may be appropriate for that to be the driver in some cases. For civil debt recovery, find ways to improve the accuracy of contact information for registered vehicle owners. Noting that debt collection agencies seem to be able to find debtors easier that toll road operators. Toll road operators should develop and publish customer charters

- Rate setting/tolling policy

- Business rules

- Competition

- Governance